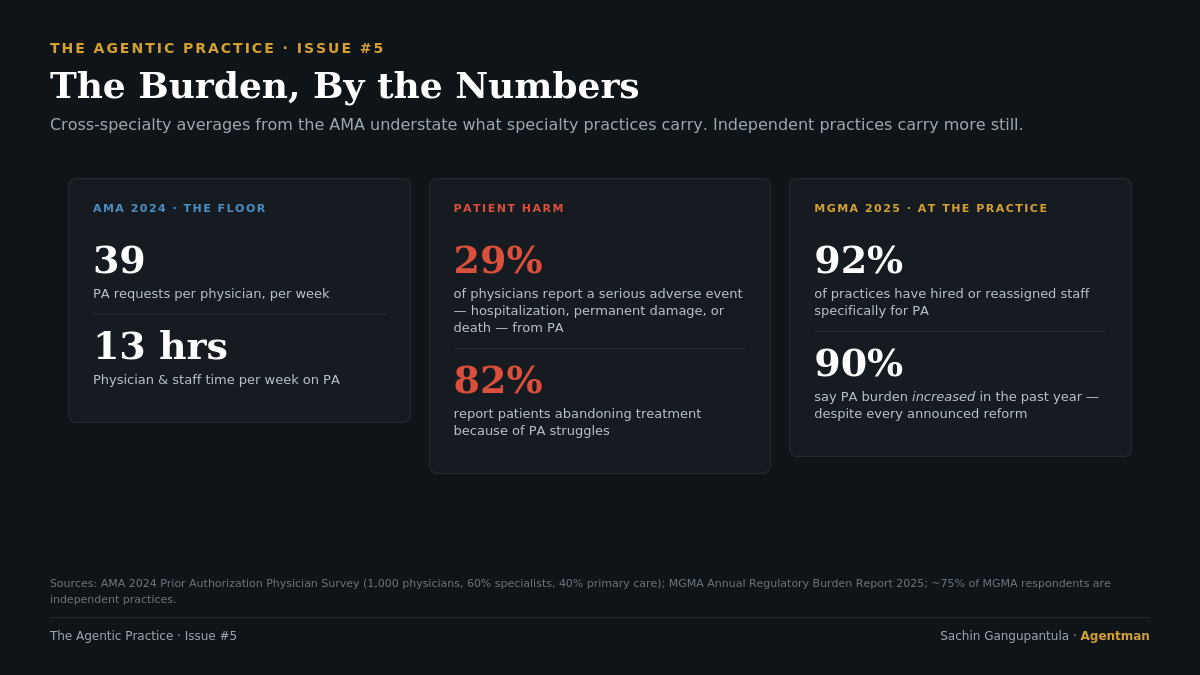

Last year, the average physician spent 13 hours a week on prior authorization. Two full work days. Each physician submitted 39 PA requests on average. 89% reported it was contributing to burnout. 82% had watched patients abandon recommended treatment because of PA struggles. And 29% — nearly one in three — reported a patient in their care experiencing a serious adverse event because of PA: hospitalization, permanent damage, or death.

Those numbers come from the AMA's 2024 physician survey. They're not news to anyone running a practice.

In January 2024, the federal government finally concluded that the prior authorization market had failed. CMS issued the Interoperability and Prior Authorization Final Rule (CMS-0057-F): faster decision deadlines, specific written denial reasons, mandatory public reporting, and a 2027 API requirement that would force payers to accept electronic submissions in real time. In October 2025, California followed. Governor Newsom signed SB 306 — the Defending Physicians Decisions Act — which by 2028 will eliminate prior authorization for any service a payer already approves at least 90% of the time.

Both interventions are real. They share a structural feature: they were written for payers, not for the independent practice that bears the most damage. The federal rule mandates APIs an independent practice will never operationalize on its own. The state rule, when it takes effect, will only eliminate PA for services payers were already approving. And drug PA — the entire bucket that defines our daily reality at Valley Diabetes & Obesity — is excluded from the federal rule's most consequential requirement.

I run operations at an independent primary care and diabetes practice. The patient with an HbA1c of 8.4 sitting on my schedule next Tuesday, waiting on a GLP-1 prior authorization that's now in its third week, gets nothing from either reform today. She might get something from them in 2028.

This piece is about why every "solution" the market has shipped over the last decade has the same gap baked into its design.

Table of Contents

- Where does the prior auth burden actually concentrate?

- Who was each prior auth solution actually built for?

- What did the CMS public data round reveal in 2026?

- Why is prior authorization itself the product?

- What happens to the patient who stops calling?

- What can independent practices actually do about prior authorization?

- Frequently Asked Questions

Where does the prior auth burden actually concentrate?

The AMA's averages — 39 PAs per physician per week, 13 staff hours, 89% reporting burnout — are the floor, not the ceiling. They include psychiatry, physical therapy, and primary care, where PA volume is structurally lower. The specialties built around chronic and specialty medications — rheumatology, oncology, endocrinology, dermatology, gastroenterology, neurology — carry significantly more.

40% of physicians have hired staff who work exclusively on prior authorizations. A job title that didn't exist a decade ago is now standard practice infrastructure.

The MGMA Annual Regulatory Burden Report for 2025 — where roughly three-quarters of respondents work at independent practices — found 92% have hired or reassigned staff specifically for PA, 60% report three or more employees per request, and 90% saw the burden increase over the past year. Despite every announced reform.

The independent specialty practice sits at the bottom of both stratifications: highest PA burden by specialty, lowest leverage by structure. Every "solution" the industry has built has reached this tier last, if at all.

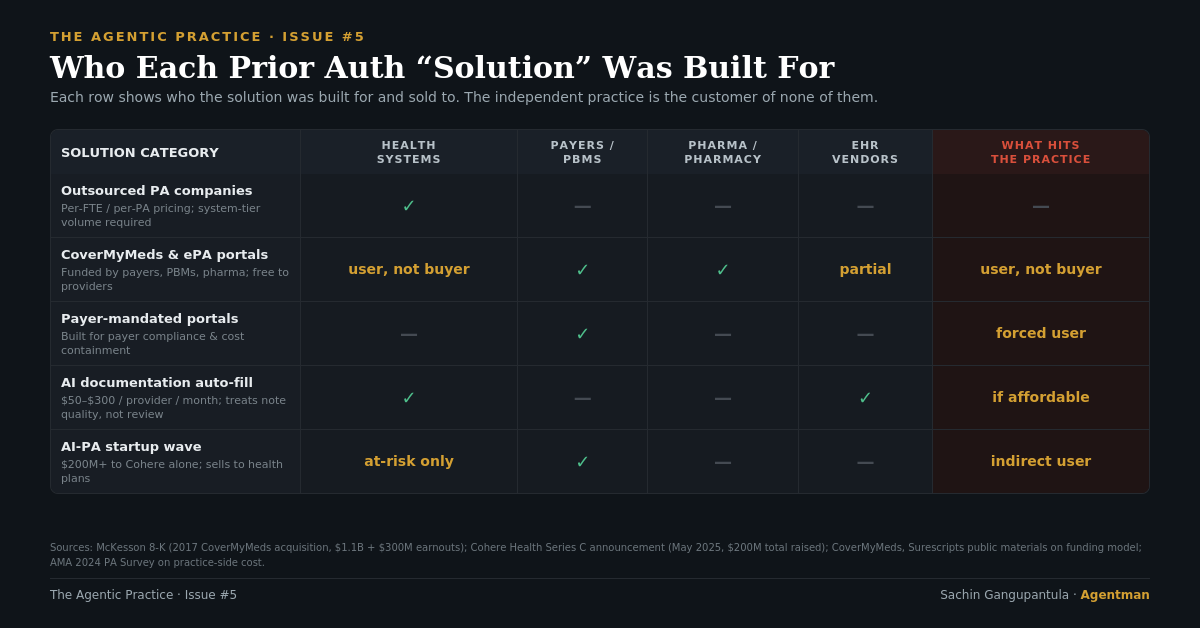

Who was each prior auth solution actually built for?

Every prior authorization solution shipped over the past decade was financed by, designed for, or sold to the payer side of the market — not the independent practice that bears the most damage. The five categories below are the ones a typical practice operator will encounter when shopping for relief, and the buyer behind each one explains why none of them actually closes the gap.

1. Outsourced PA companies

Hire a vendor to do the work for you. Industry pricing reveals the intended buyer: $7 per electronic PA on the low end, $35–$100 per complex manual PA. A specialty practice handling AMA-average volume looks at $14,000 to $70,000 per physician per year, before specialty surcharges. For a five-physician diabetes practice, that's $70,000 to $350,000 per year. The math only pencils with system-tier volume to negotiate against. Independent specialty practices typically don't have it.

2. CoverMyMeds and the EHR-integrated category

CoverMyMeds is the most-cited PA tool in the industry. McKesson acquired it in 2017 for $1.1 billion plus up to $300 million in earnouts. It is free to providers — funded by health plans, PBMs, and pharmaceutical manufacturers.

We deployed it at Valley Diabetes & Obesity. It didn't replace anything. The fax line stayed. Pharmacies that initiate PAs on CoverMyMeds send yet another fax about it. Most major payers in our market mandate their own portal for the medications they intend to scrutinize most heavily — which in diabetes care means GLP-1s, CGMs, and long-acting insulins. The "EHR-integrated" framing only holds if your EHR has the integration brokered. Smaller, less expensive EHRs have weaker coverage; the standalone fallback is yet another portal to log into and train every new MA on.

Free does not mean costless. The cost was redistributed onto the practice's staff and the physician.

3. Payer ePA portals and Availity

Each major payer maintains its own portal, or operates on Availity. From an independent practice's perspective, this is portal proliferation that scales linearly with payer mix. We contract with most of the major national and regional payers. That's most of the major portals to maintain, each with its own login, clinical question sets, appeals process, and quirks. The cost isn't on the invoice. It's on the staff schedule, and it grows with every new payer contract.

4. AI documentation auto-fill

EHR-adjacent vendors ship AI tools that write better-formatted PA submissions by pulling structured data from clinical notes. Pricing runs $50 to $300 per provider per month, plus integration overhead. The category solves a real problem — but addresses the wrong bottleneck. A better-formatted submission to the same review process produces a faster, more legible denial.

5. The AI-PA startup wave

The largest funding wave in healthcare AI over the past two years has been deployed into prior authorization automation. Cohere Health has raised $200 million and describes itself as "the leader in clinical intelligence solutions for health plans." Rhyme has raised approximately $58 million. Banjo, Anterior, Alaffia, Develop Health and a dozen others occupy adjacent positions.

Read the first sentence of any of their company descriptions. The buyer is the payer.

Independent practices are not the customer, not the contract, and in most deployments not even a meaningful end-user. Cohere's own January 2026 announcement uses the phrase "AI ping-pong with providers" — payer-side automation now arriving fast enough that providers are deploying their own AI to respond, in an escalating loop the patient does not benefit from. The infrastructure war is being financed on both sides.

The bedside is not.

What did the CMS public data round reveal in 2026?

CMS-0057-F's first public reporting deadline was March 31, 2026. For the first time, payers had to publish actual PA approval rates, denial rates, appeal overturn rates, and decision processing times for calendar year 2025. The data confirmed what independent practice staff schedules have shown for years: denial rates are operational policy, not clinical inevitability.

| Signal | Data Point | Source |

|---|---|---|

| Medicare Advantage PA determinations issued in 2024 | ~53 million | KFF, January 2026 |

| Medicare Advantage denials in 2024 | 4.1 million | KFF, January 2026 |

| MA appealed denials ultimately overturned | >80% | KFF, January 2026 |

| ACA marketplace in-network claim denial rate (2024) | 19% | KFF Marketplace Analysis, 2026 |

| ACA denied claims that are ever appealed | <1% | KFF Marketplace Analysis, 2026 |

| ACA internal appeals that overturn the denial | 44% | KFF Marketplace Analysis, 2026 |

| ACA denial rate variance across 175 reporting plans | 2% to 49% | KFF Marketplace Analysis, 2026 |

The Medicare Advantage data lands first. Insurers received nearly 53 million PA determinations in 2024, denying 4.1 million. More than 80% of appealed denials were ultimately overturned — and that figure has been consistently above 80% for years. If initial denials reflected sound clinical judgment, that overturn rate would be near zero. Not above 80%.

The ACA marketplace data is starker. Insurers on HealthCare.gov denied 19% of in-network claims in 2024. Only 5% of denials cited lack of medical necessity — the dominant stated reasons were "Other" (36%) and administrative (25%). Fewer than 1% of denied claims are ever appealed. Yet 44% of internal appeals overturn the denial. Across 175 reporting plans, denial rates ranged from 2% to 49%. Same regulatory environment, twenty-five-fold difference.

What does payer-side AI actually produce? A 2024 Senate report found that skilled nursing facility stays were refused nine times more often after Medicare Advantage plans adopted AI tools. Not 9% more often. Nine times. UnitedHealth and Humana now face active lawsuits over algorithmic wrongful denial. CMS in 2025 declined to issue formal rules regulating AI use in PA. California is the only state that prohibits insurers from using AI alone to make coverage decisions.

And the equity data? CMS analysis showed Medicare Advantage beneficiaries dually eligible for Medicaid face denial rates up to twice those of non-dual enrollees. The CY2025 final rule would have required public reporting of denial rates by population. The Trump administration in June 2025 announced it would not enforce that requirement. The data will continue to exist. The accountability mechanism will not.

This is a tax on your exhaustion. Payers aren't betting on clinical accuracy — they're betting on the fact that you and your staff are too burnt out to fight back. (See Newsletter #4 for the physician-side weight of that exhaustion.) When only 1% of denials are ever appealed, the Prior Auth Trap is wildly profitable. They count on us folding. Every time we don't appeal a wrongful denial, we're paying a subsidy to the payer's bottom line.

Why is prior authorization itself the product?

McKesson did not pay $1.1 billion for CoverMyMeds because providers were going to pay for it. The value flows from PBMs, payers, and pharma — the buyers — back to McKesson. The practice provides the labor that makes the data flow valuable.

The federal data confirms what the capital flows already implied. The smartest money in healthcare spent the last decade refining the prior authorization machine. The first round of public data shows what that produces: 80%+ overturn rates, 9x increases in post-acute care denials after AI adoption, 25-fold variance across plans operating under identical rules.

None of this is failing. It's all working exactly how it was designed. It just wasn't designed for us.

What happens to the patient who stops calling?

Her HbA1c was 8.4. She was 58, recently widowed, working two jobs, and one of the most committed patients I've watched walk through our doors in the last two years. Her physician prescribed a GLP-1 — the right drug for the right patient. The prior authorization went out the same day.

The first portal returned a coverage gap. The fallback portal accepted the submission, then asked for documentation we had already attached. The peer-to-peer was scheduled and rescheduled. Two weeks in, the request was denied for a reason that didn't match the payer's own published policy. We appealed. The appeal triggered another peer-to-peer with a reviewer almost certainly not a board-certified specialist.

She called every few days for the first three weeks. Then every week. Then she called once more, almost apologetically, to ask if there was any update. We told her we were still working on it. We were. We have a staff member whose entire job is working on it.

She didn't call again.

We don't have data on patients who stop calling. Nobody does. That's the part of the system nobody's measuring. And it's the part of the system that's actually failing.

What can independent practices actually do about prior authorization?

Every independent practice operator reading this already knows most of what this article said. We've lived it. The federal data just confirmed what our staff schedules have been telling us for years.

Here is the part the data did not name. The same technology being deployed against us — agentic AI built to scale denials, faster, at lower cost per denial — is the only counterweight that scales. The payers built theirs. The vendors built theirs. The venture capital found theirs. Independent practices have been waiting to be served by someone else's. We will be waiting forever.

The orphan tier does not get rescued. The orphan tier gets organized.

Three actions are available to a practice this quarter:

- Measure your real PA workload by payer and drug class. Track every PA initiated for 30 days — drug, payer, time-to-decision, denial reason, appeal outcome. Most practices underestimate volume by 30–40% and have no visibility into which payer-drug combinations cost the most labor per dollar collected.

- Identify the denial categories you've stopped appealing. That is where recoverable revenue is sitting — and where the payer is counting on your exhaustion. The 80%+ overturn rate on appealed Medicare Advantage denials tells you what is on the table.

- Evaluate agentic AI systems that execute PA workflows end-to-end on the practice's side. The test is the same one we apply to every other layer of the administrative stack: does the system execute the workflow, or does it just help your staff execute it faster? Assistive tools redistribute the burden. Agentic systems remove it.

Every practice that puts AI on its own side of the table — to triage the inbox, to draft the appeal, to surface the denial pattern, to give the physician back the hour the portal stole — is one practice that has stopped absorbing the burden as if it were permanent.

The technology that broke our staff schedules is the technology that can rebuild them. On our terms this time. That is what we are building at Agentman.

Frequently Asked Questions

How many hours per week does the average physician spend on prior authorization?

The average physician spent 13 hours per week on prior authorization in 2024, according to the AMA's National Prior Authorization Survey. Each physician submitted an average of 39 PA requests per week. Specialty practices that prescribe high volumes of chronic and specialty medications — endocrinology, rheumatology, oncology, dermatology, gastroenterology, neurology — carry significantly higher PA loads than primary care averages suggest.

Why is CMS-0057-F insufficient for independent practices?

CMS-0057-F, the federal prior authorization rule finalized in January 2024, mandates faster decision deadlines, specific written denial reasons, public reporting, and a 2027 API requirement for payers. Two structural gaps limit its impact for independent practices. First, the API mandate assumes a level of integration capacity that small practices cannot operationalize on their own. Second, drug prior authorization — the largest pain category for specialty practices — is excluded from the rule's most consequential requirement. The rule was written for payers, not for the independent practice that bears the most damage.

Why don't most independent practices appeal prior authorization denials?

Two factors drive the low appeal rate. First, exhaustion: the AMA's 2024 survey found 67% of physicians who don't appeal cite past experience telling them appealing wouldn't work. Second, economics: in the ACA marketplace, fewer than 1% of denied claims are ever appealed — yet 44% of those that are appealed get overturned. Payers structure denial volume around the assumption that the practice will not have the staff capacity, time, or institutional memory to fight back. Every unappealed denial is a subsidy to the payer's bottom line.

What did the first CMS public data release in 2026 reveal about denials?

The March 31, 2026 reporting deadline produced the first public dataset on payer denial behavior. KFF analysis found Medicare Advantage insurers issued ~53 million PA determinations in 2024, denied 4.1 million, and saw more than 80% of appealed denials overturned. ACA marketplace plans denied 19% of in-network claims, with denial rates ranging from 2% to 49% across 175 reporting plans operating under identical rules. The 25-fold variance is the clearest evidence available that denial rates reflect operational policy at the payer, not clinical inevitability.

Why are AI-PA startups not solving the problem for independent practices?

The largest funding wave in healthcare AI over the past two years — Cohere Health, Rhyme, Banjo, Anterior, Alaffia, Develop Health — has gone into prior authorization automation. The buyer in nearly every case is the payer. Independent practices are not the customer, not the contract, and in most deployments not even a meaningful end-user. The result is what Cohere itself calls "AI ping-pong with providers": payer-side automation accelerates denial volume faster than practices can respond manually. The asymmetry is not solved by faster payer AI. It is solved only when the practice deploys agentic AI on its own side of the table.

What is the difference between assistive AI and agentic AI for prior authorization?

Assistive AI helps a staff member execute a PA workflow faster — better-formatted submissions, suggested clinical justifications, drafted appeals. The staff member still drives every step. Agentic AI executes the workflow end-to-end: initiates the PA, navigates the payer portal, attaches the chart documentation, monitors decision status, drafts and submits the appeal, and surfaces only the cases that genuinely require physician judgment. Assistive tools redistribute the burden. Agentic systems remove it from the practice's workflow entirely.

I'm tired of watching us absorb this burden as if it's just the cost of doing business. It isn't. Hit reply and tell me — which specific payer or drug class is doing the most damage in your office right now? Whether that's the staff hours bleeding away or the patients giving up, I want to know. That's where we start. Let's start clawing that time back.

Sachin Gangupantula, FACHE, MBA, CDH-E — VP of Practice Operations, Valley Diabetes & Obesity; Cofounder, Agentman

The Agentic Practice publishes when the practice lets me write it.